We will begin by examining some numerical and graphical summaries of the Smarket data, which is part of the {ISLR} library. This data set consists of percentage returns for the S&P 500 stock index over 1,250 days, from the beginning of 2001 until the end of 2005. For each date, the percentage returns is recorded for each of the five previous trading days, Lag1 through Lag5. Also recorded is Volume (the number of shares traded

on the previous day, in billions), Today (the percentage return on the date in question) and Direction (whether the market was Up or Down on this date).

library(ISLR)head(Smarket)

Year Lag1 Lag2 Lag3 Lag4 Lag5 Volume Today Direction

1 2001 0.381 -0.192 -2.624 -1.055 5.010 1.1913 0.959 Up

2 2001 0.959 0.381 -0.192 -2.624 -1.055 1.2965 1.032 Up

3 2001 1.032 0.959 0.381 -0.192 -2.624 1.4112 -0.623 Down

4 2001 -0.623 1.032 0.959 0.381 -0.192 1.2760 0.614 Up

5 2001 0.614 -0.623 1.032 0.959 0.381 1.2057 0.213 Up

6 2001 0.213 0.614 -0.623 1.032 0.959 1.3491 1.392 Up

The cor() function produces a matrix that contains all of the pairwise correlations among the predictors in a data set. The first command below gives an error message because the Direction variable is qualitative.

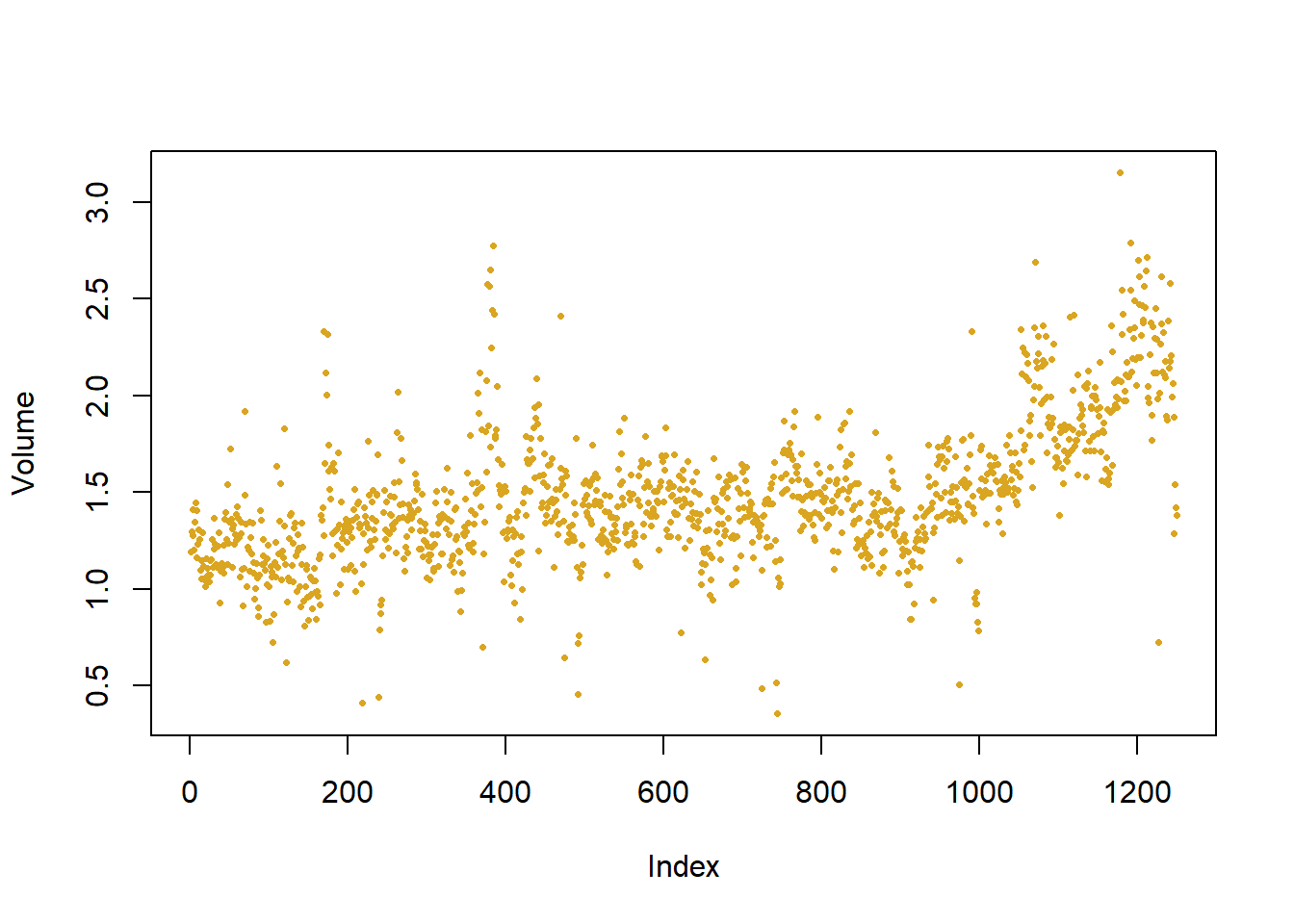

As one might expect, the correlations between the lag variables and today’s returns are close to zero. In other words, there appears to be little correlation between today’s returns and previous days’ returns. The only substantial correlation is between Year and Volume. By plotting the data we see that Volume is increasing over time. In other words, the average number of shares traded daily increased from 2001 to 2005.

attach(Smarket)plot(Volume,pch =16, col ="goldenrod", cex =0.5) # pure vanity

glm() for logistic regression

Logistic Regression is merely regression where the dependent variable is binary (up, down; yes, no; 0, 1; etc.).

We will fit a logistic regression model in order to predict Direction using Lag1 through Lag5 and Volume. The glm() function fits generalized linear models, a class of models that includes logistic regression, and allows us to model data that do not adhere to the Gaussian assumption. The syntax of the glm() function is similar to that of lm(), except that we must pass in the argument family=binomial in order to tell R to run a logistic regression rather than some other type of generalized linear model.

Call:

glm(formula = Direction ~ Lag1 + Lag2 + Lag3 + Lag4 + Lag5 +

Volume, family = binomial, data = Smarket)

Deviance Residuals:

Min 1Q Median 3Q Max

-1.446 -1.203 1.065 1.145 1.326

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -0.126000 0.240736 -0.523 0.601

Lag1 -0.073074 0.050167 -1.457 0.145

Lag2 -0.042301 0.050086 -0.845 0.398

Lag3 0.011085 0.049939 0.222 0.824

Lag4 0.009359 0.049974 0.187 0.851

Lag5 0.010313 0.049511 0.208 0.835

Volume 0.135441 0.158360 0.855 0.392

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 1731.2 on 1249 degrees of freedom

Residual deviance: 1727.6 on 1243 degrees of freedom

AIC: 1741.6

Number of Fisher Scoring iterations: 3

The smallest p-value here is associated with Lag1. The negative coefficient for this predictor suggests that if the market had a positive return yesterday, then it is less likely to go up today. However, at a value of 0.15, the p-value is still relatively large, and so there is no clear evidence of a real association between Lag1 and Direction.

We use the coef() function in order to access just the coefficients for this fitted model. We can also use the summary() function to access particular aspects of the fitted model, such as the p-values for the coefficients.

summary(glm.fit)$coef[4] # just the 4th coefficient, Lag3

[1] 0.01108511

predict()

The predict() function can be used to predict the probability that the market will go up, given values of the predictors. The type="response" option tells R to output probabilities of the form \(P(Y = 1|X)\) (the probability that Y = the value of ‘1’, given some value of X), as opposed to other information such as the logit. If no data set is supplied to the predict() function, then the probabilities are computed for the training data that was used to fit the logistic regression model. Here we can print the first ten probabilities. We know that these values correspond to the probability of the market going up, rather than down, because the contrasts() function indicates that R has created a dummy variable with a 1 for Up.

glm.probs <-predict(glm.fit, type ="response")glm.probs[1:10]

In order to make a prediction as to whether the market will go up or down on a particular day, we can convert these predicted probabilities into class labels, Up or Down. The following two commands create a vector of class predictions based on whether the predicted probability of a market increase is greater than or less than 0.5.

glm.pred <-rep("Down", 1250) # make vectorglm.pred[glm.probs > .5] <-"Up"# add Up values

table()

The first command creates a vector of 1,250 Down elements. The second line transforms to Up all of the elements for which the predicted probability of a market increase exceeds 0.5. Given these predictions, the table() function can be used to produce a confusion matrix in order to determine how many observations were correctly or incorrectly classified.

table(glm.pred, Direction) # confusion matrix

Direction

glm.pred Down Up

Down 145 141

Up 457 507

(507+145)/1250# proportion correct predictions out of 50/50 (like flipping a coin)

The diagonal elements of the confusion matrix indicate correct predictions, while the off-diagonals represent incorrect predictions. Hence our model correctly predicted that the market would go up on 507 days and that it would go down on 145 days, for a total of 507 + 145 = 652 correct predictions. The mean() function can be used to compute the fraction of days for which the prediction was correct. In this case, logistic regression correctly predicted the movement of the market 52.2% of the time.

At first glance, it appears that the logistic regression model is working a little better than random guessing. However, this result is misleading because we trained and tested the model on the same set of 1,250 observations. In other words, \(100-52.2 = 47.8\)% is the training error rate. As we have seen previously, the training error rate is often overly optimistic because it tends to underestimate the test error rate. In order to better assess the accuracy of the logistic regression model in this setting, we can fit the model using part of the data, and then examine how well it predicts the held out data. This will yield a more realistic error rate, in the sense that in practice we will be interested in our model’s performance not on the data that we used to fit the model, but rather on days in the future for which the market’s movements are unknown.

To implement this strategy, we will first create a vector corresponding to the observations from 2001 through 2004. We will then use this vector to create a “held out” data set of observations from 2005.

The object train is a vector of 1,250 elements, corresponding to the observations in our data set. The elements of the vector that correspond to observations that occurred before 2005 are set to TRUE, whereas those that correspond to observations in 2005 are set to FALSE. The object train is a Boolean vector, since its elements are TRUE and FALSE. Boolean vectors can be used to obtain a subset of the rows or columns of a matrix. For instance, the command Smarket[train, ] would pick out a submatrix of the stock market data set, corresponding only to the dates before 2005, since those are the ones for which the elements of train are TRUE. The ! symbol can be used to reverse all of the elements of a Boolean vector.

That is, !train is a vector similar to train, except that the elements that are TRUE in train get swapped to FALSE in !train, and the elements that are FALSE in train get swapped to TRUE in !train. Therefore, Smarket[!train,] yields a submatrix of the stock market data containing only the observations for which train is FALSE. That is, the observations with dates in 2005. The output above indicates that there are 252 such observations.

Model testing

We now fit a logistic regression model using only the subset of the observations that correspond to dates before 2005, using the subset argument. We then obtain predicted probabilities of the stock market going up for each of the days in our test set. That is, for the days in 2005.

Notice that we have trained and tested our model on two completely separate data sets: training was performed using only the dates before 2005, and testing was performed using only the dates in 2005. This is the whole point.

Finally, we compute the predictions for 2005 and compare them to the actual movements of the market over that time period.

Direction.2005

glm.pred Down Up

Down 77 97

Up 34 44

mean(glm.pred == Direction.2005)

[1] 0.4801587

mean(glm.pred != Direction.2005)

[1] 0.5198413

The != notation means not equal to, and so the last command computes the test set error rate. The results are rather disappointing: the test error rate is 52%, which is worse than random guessing! Of course this result is not all that surprising, given that one would not generally expect to be able to use previous days’ returns to predict future market performance. (After all, if it were easy to do so economics would not be a field of study)

2 Fine tuning models

We recall that the logistic regression model had very underwhelming p-values associated with all of the predictors, and that the smallest p-value, though not very small, corresponded to Lag1. Perhaps by removing the variables that appear not to be helpful in predicting Direction, we can obtain a more effective model. After all, using predictors that have no relationship with the response tends to cause a deterioration in the test error rate (since such predictors cause an increase in variance without a corresponding decrease in bias), and so removing such predictors may in turn yield an improvement. Below we will refit the logistic regression using just Lag1 and Lag2, which seemed to have the highest predictive power in the original logistic regression model.

glm.fit <-glm (Direction ~ Lag1 + Lag2, data = Smarket, family = binomial, subset = train)glm.probs <-predict(glm.fit, Smarket.2005, type ="response")glm.pred <-rep ("Down" ,252)glm.pred[glm.probs > .5] ="Up"table(glm.pred, Direction.2005)

Direction.2005

glm.pred Down Up

Down 35 35

Up 76 106

mean(glm.pred == Direction.2005)

[1] 0.5595238

106/(106+76)

[1] 0.5824176

Now the results appear to be a little better: 56% of the daily movements have been correctly predicted. It is worth noting that in this case, a much simpler strategy of predicting that the market will increase every day will also be correct 56% of the time! Hence, in terms of overall error rate, the logistic regression method is no better than the naïve approach. However, the confusion matrix shows that on days when logistic regression predicts an increase in the market, it has a 58% accuracy rate. This suggests a possible trading strategy of buying on days when the model predicts an increasing market, and avoiding trades on days when a decrease is predicted. Of course one would need to investigate more carefully whether this small improvement was real or just due to random chance.

More predict()

Suppose that we want to predict the returns associated with particular values of Lag1 and Lag2. In particular, we want to predict Direction on a day when Lag1 and Lag2 equal 1.2 and 1.1, respectively, and on a day when they equal 1.5 and −0.8. We do this using the predict() function.

predict(glm.fit, newdata =data.frame(Lag1 =c(1.2, 1.5),Lag2 =c(1.1, -0.8)), type ="response")

1 2

0.4791462 0.4960939

3 LDA

lda()

We use Linear Discriminant Analysis (LDA) to explore differences between data with two or more classes.

Now we will perform LDA on the Smarket data. In R, we fit a LDA model using the lda() function, which is part of the MASS library. Notice that the syntax for the lda() function is identical to that of lm(), and to that of glm() except for the absence of the family option. We fit the model using only the observations before 2005.

Call:

lda(Direction ~ Lag1 + Lag2, data = Smarket, subset = train)

Prior probabilities of groups:

Down Up

0.491984 0.508016

Group means:

Lag1 Lag2

Down 0.04279022 0.03389409

Up -0.03954635 -0.03132544

Coefficients of linear discriminants:

LD1

Lag1 -0.6420190

Lag2 -0.5135293

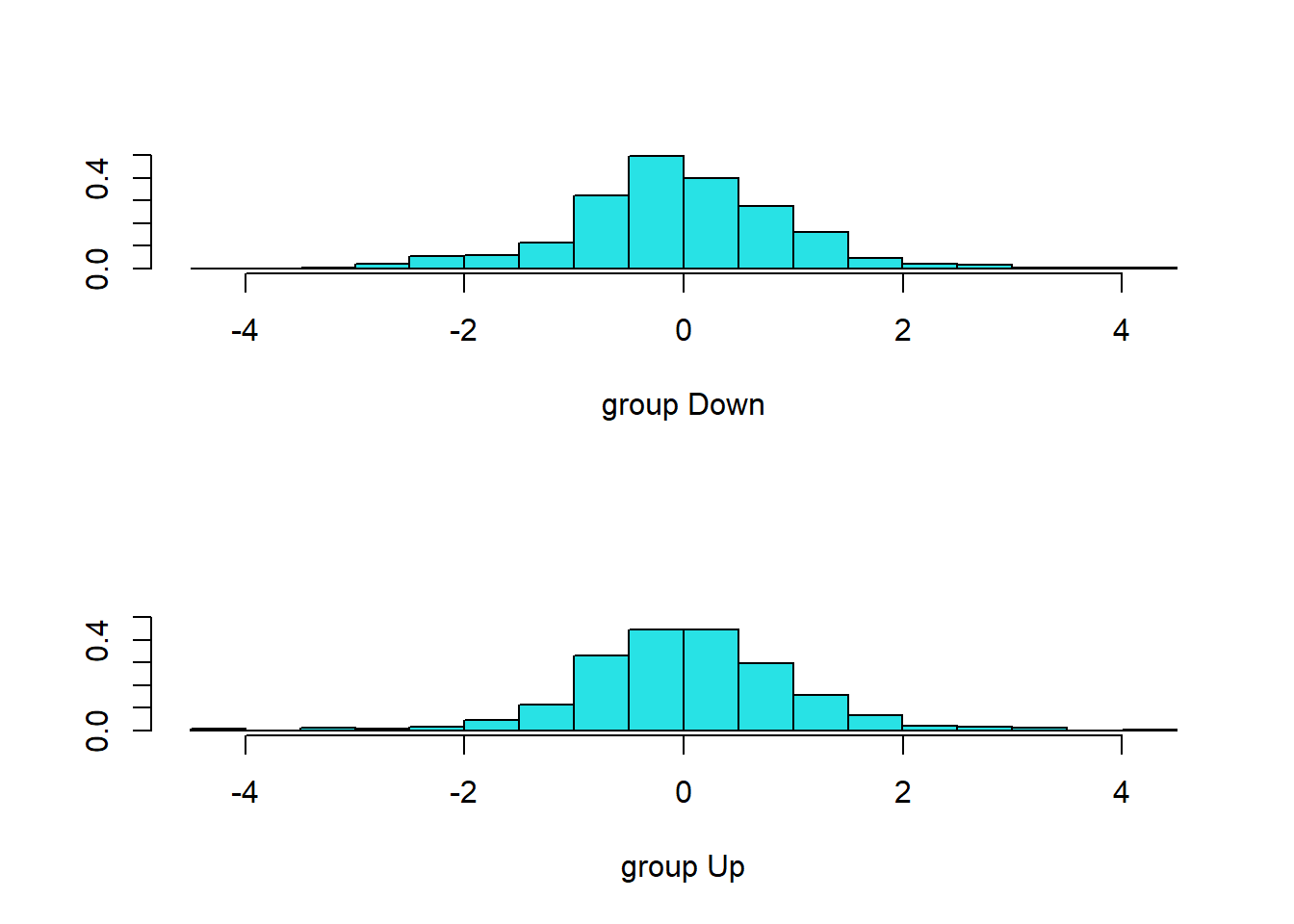

plot(lda.fit)

The LDA output indicates that \(\hat\pi_1 = 0.492\) and \(\hat\pi_2 = 0.508\); in other words, 49.2% of the training observations correspond to days during which the market went down. It also provides the group means; these are the average of each predictor within each class, and are used by LDA as estimates of \(μ_k\). These suggest that there is a tendency for the previous 2 days’ returns to be negative on days when the market increases, and a tendency for the previous days’ returns to be positive on days when the market declines. The coefficients of linear discriminants output provides the linear combination of Lag1 and Lag2 that are used to form the LDA decision rule.

In other words, these are the multipliers of the elements of X = x in (4.19). If −0.642 × Lag1− 0.514 × Lag2 is large, then the LDA classifier will predict a market increase, and if it is small, then the LDA classifier will predict a market decline. The plot() function produces plots of the linear discriminants, obtained by computing 0.642 X Lag1 - 0.514 Lag2 for each of the training observations.

The predict() function returns a list with three elements. The first element, class, contains LDA’s predictions about the movement of the market. The second element, posterior, is a matrix whose kth column contains the posterior probability that the corresponding observation belongs to the kth class. Finally, x contains the linear discriminants, described earlier.

[1] Up Up Up Up Up Up Up Up Up Up Up Down Up Up Up

[16] Up Up Down Up Up

Levels: Down Up

If we wanted to use a posterior probability threshold other than 50% in order to make predictions, then we could easily do so. For instance, suppose that we wish to predict a market decrease only if we are very certain that the market will indeed decrease on that day. Say, if the posterior probability is at least 90%.

sum(lda.pred$posterior[ , 1] > .9)

[1] 0

No days in 2005 meet that threshold! In fact, the greatest posterior probability of decrease in all of 2005 was 52.02%.

4 QDA

qda() Quadratic Discriminant Analysis

We will now fit a QDA model to the Smarket data. QDA is implemented in R using the qda() function, which is also part of the {MASS} library. The syntax is identical to that of lda().

Call:

qda(Direction ~ Lag1 + Lag2, data = Smarket, subset = train)

Prior probabilities of groups:

Down Up

0.491984 0.508016

Group means:

Lag1 Lag2

Down 0.04279022 0.03389409

Up -0.03954635 -0.03132544

The output contains the group means. But it does not contain the coefficients of the linear discriminants, because the QDA classifier involves a quadratic, rather than a linear, function of the predictors. The predict() function works in exactly the same fashion as for LDA.

Direction.2005

qda.class Down Up

Down 30 20

Up 81 121

mean(qda.class == Direction.2005)

[1] 0.5992063

Interestingly, the QDA predictions are accurate almost 60% of the time, even though the 2005 data was not used to fit the model. This level of accuracy is quite impressive for stock market data, which is known to be quite hard to model accurately. This suggests that the quadratic form assumed by QDA may capture the true relationship more accurately than the linear forms assumed by LDA and logistic regression. However, it is recommended to evaluate any method’s performance on a larger test set before betting that this approach will consistently beat the market!

5 K-Nearest Neighbors

knn()

We will now perform KNN using the knn() function, which is part of the {class} library. This function works rather differently from the other model-fitting functions that we have encountered thus far. Rather than a two-step approach in which we first fit the model and then we use the model to make predictions, knn() forms predictions using a single command. The function requires four inputs.

A matrix containing the predictors associated with the training data, labeled train.X below.

A matrix containing the predictors associated with the data for which we wish to make predictions, labeled test.X below.

A vector containing the class labels for the training observations, labeled train.Direction below.

A value for K, the number of nearest neighbors to be used by the classifier.

We will use the cbind() function, short for column bind, to bind the Lag1 and Lag2 variables together into two matrices, one for the training set and the other for the test set.

Now the knn() function can be used to predict the market’s movement for the dates in 2005. We set a random seed before we apply knn() because if several observations are tied as nearest neighbors, then R will randomly break the tie. Therefore, a seed must be set in order to ensure reproducibility of results.

set.seed(1)library(class)knn.pred <-knn(train.X, test.X, train.Direction, k =1)table(knn.pred, Direction.2005)

Direction.2005

knn.pred Down Up

Down 43 58

Up 68 83

(83+43) /252

[1] 0.5

The results using K = 1 are not very good, since only 50% of the observa- tions are correctly predicted. Of course, it may be that K = 1 results in an overly flexible fit to the data. Let’s repeat the analysis using a different K, K = 3.

knn.pred <-knn(train.X, test.X, train.Direction, k =3)table(knn.pred, Direction.2005)

Direction.2005

knn.pred Down Up

Down 48 54

Up 63 87

mean (knn.pred == Direction.2005)

[1] 0.5357143

The results have improved slightly. But increasing K further turns out to provide no further improvements. It appears that for this data, QDA provides the best results of the methods that we have examined so far.

Caravan insurance data

Finally, we will apply the KNN approach to the Caravan data set, which is part of the {ISLR} library. This data set includes 85 predictors that measure demographic characteristics for 5,822 individuals. The response variable is Purchase, which indicates whether or not a given individual purchases a caravan insurance policy. In this data set, only 6% of people purchased caravan insurance.

dim(Caravan)

[1] 5822 86

attach(Caravan)summary(Purchase)

No Yes

5474 348

348/5822# % purchasing insurance

[1] 0.05977327

Because the KNN classifier predicts the class of a given test observation by identifying the observations that are nearest to it, the scale of the variables matters. Any variables that are on a large scale will have a much larger effect on the distance between the observations, and hence on the KNN classifier, than variables that are on a small scale. For instance, imagine a data set that contains two variables, salary and age (measured in dollars and years, respectively). As far as KNN is concerned, a difference of $1,000 in salary is enormous compared to a difference of 50 years in age. Consequently, salary will drive the KNN classification results, and age will have almost no effect. This is contrary to our intuition that a salary difference of $1,000 is quite small compared to an age difference of 50 years. Furthermore, the importance of scale to the KNN classifier leads to another issue: if we measured salary in British Pounds, or if we measured age in minutes, then we’d get quite different classification results from what we get if these two variables are measured in dollars and years.

Standardizing data

A good way to handle this problem is to standardize the data so that all variables are given a mean of zero and a standard deviation of one. Then all variables will be on a comparable scale. The scale() function does just this. In standardizing the data, we exclude column 86, because that is the qualitative Purchase variable.

Now every column of standardized.X has a standard deviation of one and a mean of zero.

We now split the observations into a test set, containing the first 1,000 observations, and a training set, containing the remaining observations. We fit a KNN model on the training data using K = 1, and evaluate its performance on the test data.

test <-1:1000train.X <- standardized.X[-test, ]test.X <- standardized.X[test, ]train.Y <- Purchase[-test]test.Y <- Purchase[test]set.seed(1)knn.pred <-knn(train.X, test.X, train.Y, k =1)mean(test.Y != knn.pred )

[1] 0.118

mean(test.Y !="No")

[1] 0.059

The vector test is numeric, with values from 1 through 1,000. Typing standardized.X[test, ] yields the submatrix of the data containing the observations whose indices range from 1 to 1,000, whereas typing standardized.X[-test, ] yields the submatrix containing the observations whose indices do not range from 1 to 1,000. The KNN error rate on the 1,000 test observations is just under 12%. At first glance, this may appear to be fairly good. However, since only 6% of customers purchased insurance, we could get the error rate down to 6% by always predicting No regardless of the values of the predictors!

Suppose that there is some non-trivial cost to trying to sell insurance to a given individual. For instance, perhaps a salesperson must visit each potential customer. If the company tries to sell insurance to a random selection of customers, then the success rate will be only 6%, which may be far too low given the costs involved. Instead, the company would like to try to sell insurance only to customers who are likely to buy it. So the overall error rate is not of interest. Instead, the fraction of individuals that are correctly predicted to buy insurance is of interest.

It turns out that KNN with K = 1 does far better than random guessing among the customers that are predicted to buy insurance. Among 77 such customers, 9, or 11.7%, actually do purchase insurance. This is double the rate that one would obtain from random guessing.

table(knn.pred, test.Y)

test.Y

knn.pred No Yes

No 873 50

Yes 68 9

9/(68+9)

[1] 0.1168831

Exploring KNN model tuning

Using K = 3 (implying there are 3 groupings of customers), the success rate increases to 19%, and with K = 5 (5 groups) the rate is 26.7%. This is over four times the rate that results from random guessing. It appears that KNN is finding some real patterns in a difficult data set!

knn.pred <-knn(train.X, test.X, train.Y, k =3)table(knn.pred, test.Y)

test.Y

knn.pred No Yes

No 920 54

Yes 21 5

5/26

[1] 0.1923077

knn.pred <-knn(train.X, test.X, train.Y, k =5)table(knn.pred, test.Y)

test.Y

knn.pred No Yes

No 930 55

Yes 11 4

4/15

[1] 0.2666667

Compare to logistic regression

As a comparison, we can also fit a logistic regression model to the data. If we use 0.5 as the predicted probability cut-off for the classifier, then we have a problem: only seven of the test observations are predicted to purchase insurance. Even worse, we are wrong about all of these! However, we are not required to use a cut-off of 0.5. If we instead predict a purchase any time the predicted probability of purchase exceeds 0.25, we get much better results: we predict that 33 people will purchase insurance, and we are correct for about 33% of these people. This is over five times better than random guessing!

glm.fit <-glm(Purchase ~ ., data = Caravan, family = binomial,subset =-test)

Warning: glm.fit: fitted probabilities numerically 0 or 1 occurred

The next few questions should be answered using the Weekly data set, which is part of the {ISLR2} package. (read about it in help())

1.1

Produce some numerical and graphical summaries of the Weekly data. Do there appear to be any patterns?

1.2

Use the full data set to perform a logistic regression with Direction as the response and the five lag variables plus Volume as predictors. Use the summary function to print the results. Do any of the predictors appear to be statistically significant? If so, which ones?

1.3

Compute the confusion matrix and overall fraction of correct predictions. Explain what the confusion matrix is telling you about the types of mistakes made by logistic regression.

1.4

Now fit the logistic regression model using a training data period from 1990 to 2008, with Lag2 as the only predictor. Compute the confusion matrix and the overall fraction of correct predictions for the held out data (that is, the data from 2009 and 2010).

1.5

Repeat 1.4 using LDA.

1.6

Repeat 1.4 using QDA.

1.7

Repeat 1.4 using KNN with K = 1.

1.8

Repeat 1.4 using naive Bayes.

1.9

Which of these methods appears to provide the best results on this data?

1.10

Experiment with different combinations of predictors, including possible transformations and interactions, for each of the methods. Report the variables, method, and associated confusion matrix that appears to provide the best results on the held out data. Note that you should also experiment with values for K in the KNN classifier.